Macro Signposts | 16 July 2025

The Economic Impact of

U.S. Tariffs: Waiting, Watching, and Planning

Since

January, the Trump administration has imposed broad tariffs - both across-the-board and targeted - with

more likely to follow. At the same time, Congress - with the administration's encouragement - has passed

legislation to reduce business and household income taxes.

When and how the U.S. economy

adjusts to this new regime is still an open question.

Current conventional wisdom is that

domestic households ultimately will pay a good portion of the tariffs as businesses charge higher prices

to offset the higher cost of imports. In turn, higher prices that reduce disposable incomes are expected

to reduce real consumption and weigh on near-term economic activity. Over time, greater incentives to

invest domestically could provide an offset.

However, after three months of higher tariffs,

data suggest that businesses' pass-through of higher tariffs via higher prices has been slow and uneven.

Corporate profits appear to be absorbing more of the additional costs, at least so far. While businesses

could still adjust prices and labor costs, which could weigh on aggregate incomes, the post-pandemic

surge in corporate margins and the front-loaded tax incentives in the One Big Beautiful Bill Act (OBBB)

may prompt more gradual adjustments.

The upshot is that the near-term impact of this year's

policy changes - slower growth, higher inflation - could be milder than expected, making it easier for

the Federal Reserve to resume its shift toward neutral monetary policy. The downside is that lower

corporate profits could lead to tighter financial conditions before the new tax and tariff regime

incentives foster the capital expenditures needed for the economy to shift away from its reliance on

consumption.

History provides a guide

The scale and scope of the Trump

administration's tariff policies are unprecedented in modern times. These policies have already raised

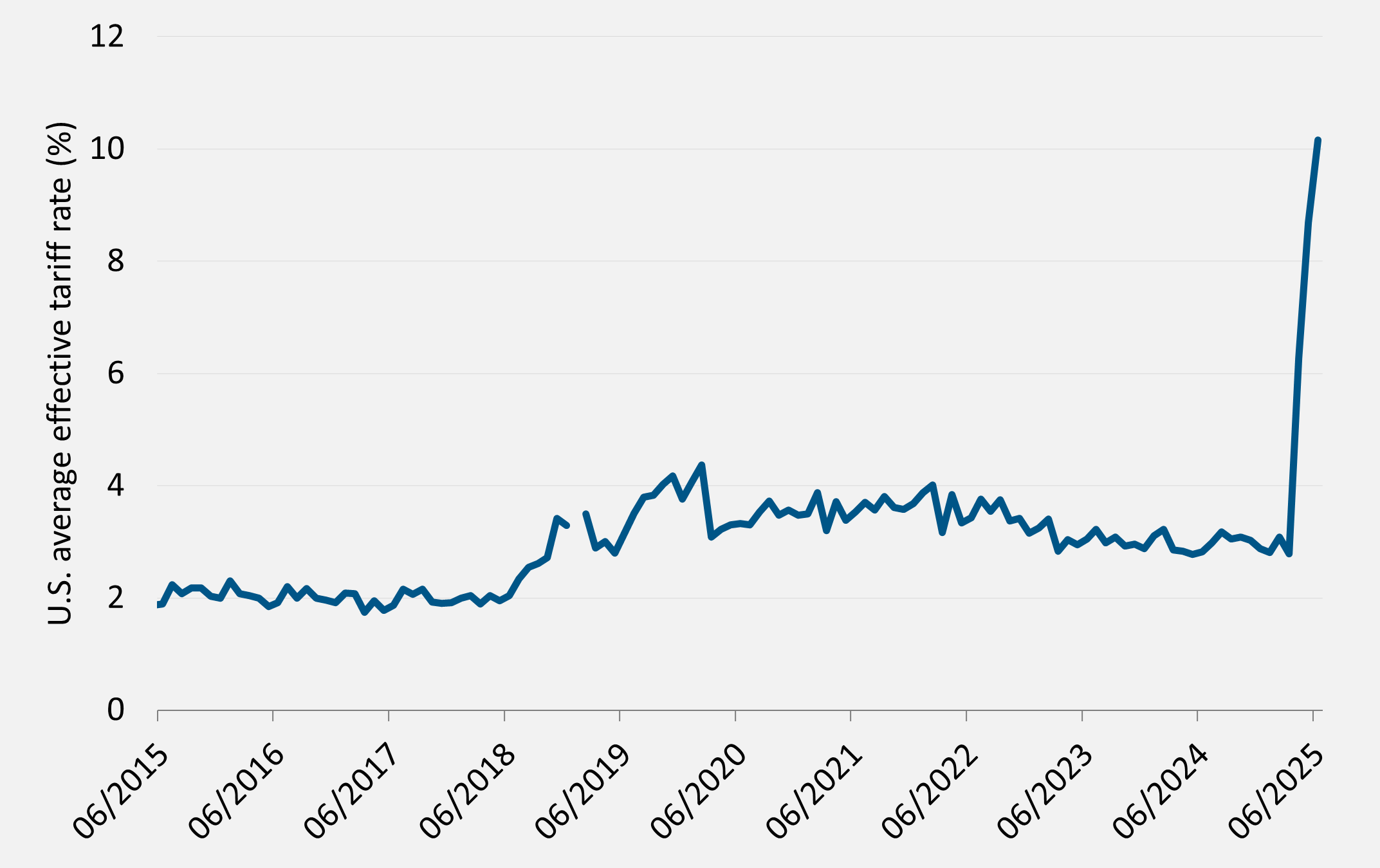

the average effective tariff rate that the U.S. currently charges on imports to roughly 11% (from less

than 3% in 2024 - see Figure 1), based on Treasury data. In the second half of the year, we expect that

number to increase further when additional sectoral and possibly higher reciprocal tariffs are

implemented. The closest analog for an industrial economy is the Smoot-Hawley Tariff Act of 1930,

designed to protect American farmers and manufacturers from foreign competition. It boosted the

effective U.S. tariff rate from less than 10% to about 20%.

Figure 1: The effective U.S. tariff rate has risen dramatically in

2025

|

Source:

U.S. Treasury Department and PIMCO calculations as of June 2025. Effective tariff rate is based on

Treasury collections.

Signals in recent U.S. economic data

While history provides a potential guide, we also have several months of data to signal how the U.S. economy is actually adjusting to this year's tariff policies. Based on observations from various official data sources, we conclude that consumer pass-through has been slower and more uneven across industries. Overall, companies appear to be paying the bulk of the higher tariff-related taxes so far, although there is some evidence of attempts to maintain profits through lower import prices and lower labor cost growth. Consider the following economic data:

- Treasury import excise tax collections and census reported duties: Treasury's daily cash statement reports significant tariff revenue collections, despite media reports of business strategies to evade tariffs. June collections were on pace for about $350 billion annualized. Data from the U.S. Census Bureau, which calculates duties based on detailed tariff schedules applied to product- and country-level imports, appears consistent with large actual collections. Both datasets suggest the average effective tariff rate on all U.S. imports is roughly 11% as of June.

- Consumer Price Index: In June, companies began more aggressively passing on the cost of tariffs through consumer goods price hikes. However, the change in goods price inflation from the beginning of the year suggests only about 20% of the total potential price pass-through has happened. Core goods price inflation has accelerated by 1 percentage point (ppt) since January, despite a fall in auto prices.

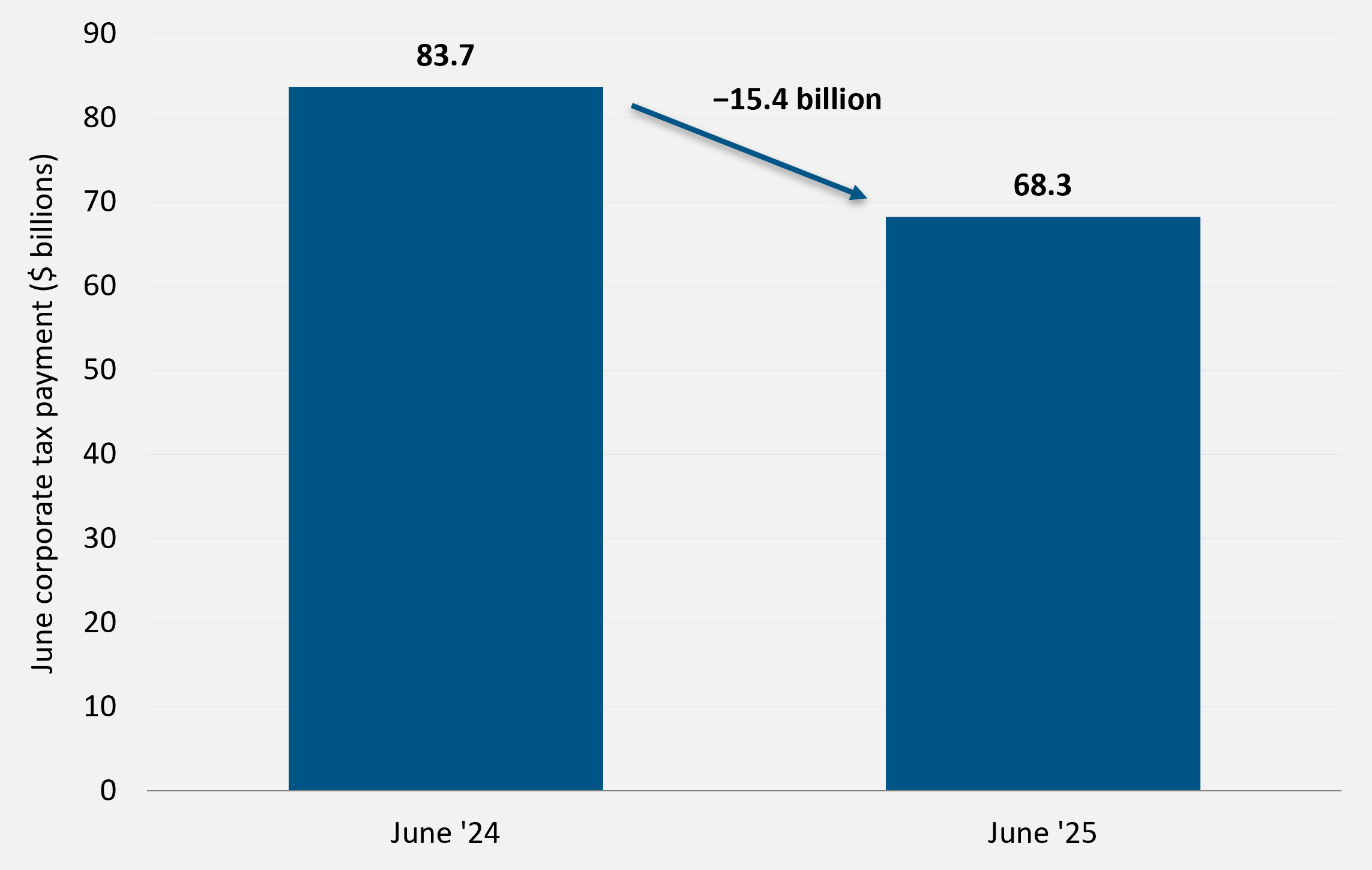

- Treasury corporate income tax payments: Treasury's daily cash statement reported that June corporate income tax payments fell below $70 billion annualized (see Figure 2). That amount is similar to 20% of the roughly $300 billion in annualized tariff revenue the Treasury collected for the second quarter - nearly matching the expected decline if firms absorbed most additional tariff costs.

Figure 2: Tax revenue suggests companies have borne the brunt of tariffs

|

Source:

Haver Analytics as of 30 June 2025. PIMCO does not provide legal or tax advice. Please consult your

tax and/or legal counsel for specific tax or legal questions and concerns.

- Employment Situation Report: June U.S. labor market data showed a contraction in aggregate hours and real incomes, while travel industry data suggest that companies are also cutting back on business travel to reduce costs.

- Import Price Index: While Japan has reported lower prices of auto exports to the U.S., and U.S.-reported Chinese import deflation has recently accelerated, broader U.S. import prices have contracted about 1% year-over-year since the beginning of 2025 - nowhere near enough to offset the 11% average effective tariff rate increase. Furthermore, the roughly 6% depreciation in the U.S. dollar year-to-date should make foreign imports more expensive in U.S. dollar terms.

What is the outlook for this to continue? Comparing additional tariffs against domestic aggregated profits reported in the National Income and Product Accounts (NIPA) suggests that tariffs could result in a large one-time hit to corporate profits if fully absorbed. According to NIPA, the estimated $350 billion in annualized tariff revenue equates to around 11% of after-tax profits, or 9% of pre-tax profits.

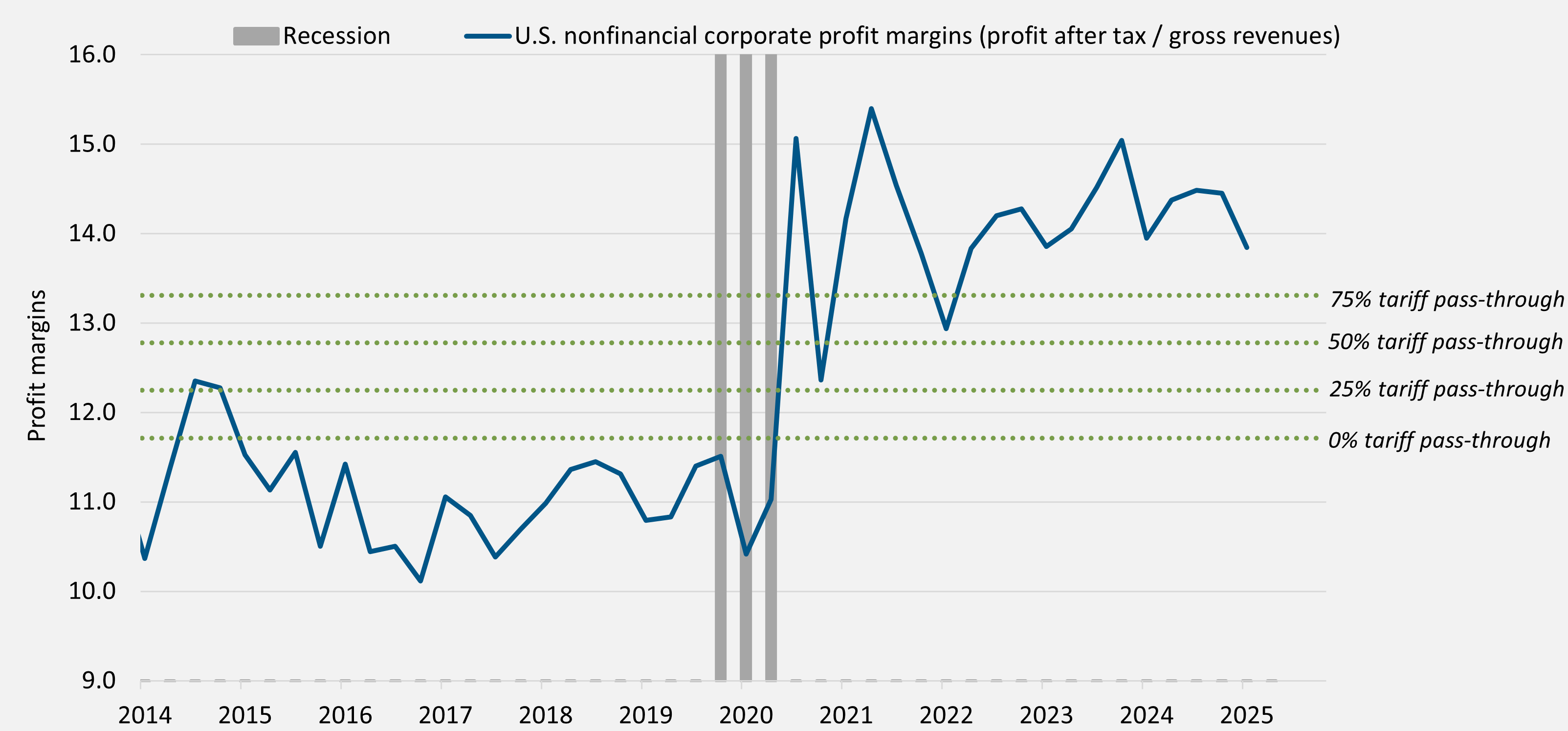

However, the post-pandemic surge in margins argues for some room for businesses to absorb near-term costs. A full absorption would lower economywide corporate margins by around 2 ppts, back to pre-pandemic levels, according to NIPA data (see Figure 3).

Figure 3: U.S. corporate profit margins under different tariff pass-through assumptions

|

Source:

U.S. National Income and Product Accounts (NIPA) as of Q1 2025

Legal questions further complicate the tariff outlook, and this means larger businesses able to weather the near-term corporate margin hit could continue a gradual pace of tariff-related adjustments. In May, the U.S. Court of International Trade (CIT) found that President Donald Trump's use of the 1977 International Emergency Economic Powers Act (IEEPA) to implement sweeping tariffs exceeded the law's authority. The Supreme Court could rule on the case later this year. Should the Supreme Court uphold the CIT's decision, the Treasury might need to refund all collected tariff revenue. The Trump administration could pursue alternative tariff measures under Section 301 and 232 investigations, which are more resilient to legal challenge, but require additional time.

For the Fed, evidence of slower pass-through that may mitigate peak inflation has to be good news, even if somewhat higher goods inflation is more persistent beyond this year.

U.S. households could be relatively better off if the higher burden of tariffs compounds gradually over time. However, there's also a risk that near-term corporate profit weakness to surprise investors and tighten financial conditions before longer-term investments can be made.

Catch up on recent editions of Macro Signposts:

- Developed Market Public Debt: A Long Road Ahead | 24 June 2025

- U.S. Policy Watch: From Trade to Taxes | 18 June 2025

- PIMCO Secular Outlook Key Takeaways: The Fragmentation Era | 10 June 2025

- Japan: Rates and Risks Back on the Global Stage | 3 June 2025

- The U.S. Current Account: Trade and Fiscal Deficits Are Closely Linked | 28 May 2025

Not

yet subscribed? To receive Macro Signposts each week, please sign up here. Macro Signposts highlights weekly takeaways from the data

analysis conducted by our team of economists and other macro experts. For PIMCO's official views

on the global economy, please visit pimco.com.

We welcome your questions about

the global macro landscape. Don't hesitate to suggest themes or data for us to analyze and

discuss: Please email [email protected].

For regular insights on U.S. policy via email, please sign up here to receive PIMCO Washington Watch from Libby Cantrill,

head of public policy.

All

investments contain risk and may lose

value.

Statements concerning financial market trends or portfolio

strategies are based on current market conditions, which will fluctuate.

There is no guarantee that these investment strategies will work under all

market conditions or are appropriate for all investors and each investor

should evaluate their ability to invest for the long term, especially during

periods of downturn in the market. Investors should consult their investment

professional prior to making an investment decision. Outlook and strategies

are subject to change without notice.

This material contains the

current opinions of the author and such opinions are subject to change

without notice. This material is distributed for informational purposes only

and should not be considered as investment advice or a recommendation of any

particular security, strategy or investment product. Information contained

herein has been obtained from sources believed to be reliable, but not

guaranteed.

PIMCO as a general matter provides services to

qualified institutions, financial intermediaries and institutional

investors. Individual investors should contact their own financial

professional to determine the most appropriate investment options for their

financial situation. This is not an offer to any person in any jurisdiction

where unlawful or unauthorized. | Pacific Investment Management

Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660

is regulated by the United States Securities and Exchange Commission. |

PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U

3AH, United Kingdom) is authorised and regulated by the

Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in

the UK. The services provided by PIMCO Europe Ltd are not available to

retail investors, who should not rely on this communication but contact

their financial adviser. Since PIMCO Europe Ltd services and products are

provided exclusively to professional clients, the appropriateness of such is

always affirmed. PIMCO Europe GmbH (Company No. 192083, Seidlstr.

24-24a, 80335 Munich, Germany) is authorized and regulated by

the German Federal Financial Supervisory Authority (BaFin) (Marie-

Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with

Section 15 of the German Securities Institutions Act (WpIG). PIMCO

Europe GmbH Italian Branch (Company No. 10005170963, Via Turati nn.

25/27 (angolo via Cavalieri n. 4) 20121 Milano, Italy), PIMCO Europe

GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02

F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11

Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch

(N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046

Madrid, Spain), PIMCO Europe GmbH French Branch (Company No. 918745621

R.C.S. Paris, 50-52 Boulevard Haussmann, 75009 Paris, France) and PIMCO

Europe GmbH (DIFC Branch) (Company No. 9613, Unit GD-GB-00-15-BC-05-0,

Level 15, Gate Building, Dubai International Financial Centre, United

Arab Emirates) are additionally supervised by: (1)

Italian Branch: the Commissione Nazionale per le Società e la Borsa

(CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in

accordance with Article 27 of the Italian Consolidated Financial Act; (2)

Irish Branch: the Central Bank of Ireland (New Wapping

Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43

of the European Union (Markets in Financial Instruments) Regulations 2017,

as amended; (3) UK Branch: the Financial Conduct Authority

(FCA) (12 Endeavour Square, London E20 1JN); (4)

Spanish Branch: the Comisión Nacional del Mercado de Valores

(CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations

stipulated in articles 168 and 203 to 224, as well as obligations contained

in Tile V, Section I of the Law on the Securities Market (LSM) and in

articles 111, 114 and 117 of Royal Decree 217/2008, respectively, (5)

French Branch: ACPR/Banque de France (4 Place de Budapest,

CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive

2014/65/EU on markets in financial instruments and under the surveillance of

ACPR and AMF and (6) DIFC Branch: Regulated by the Dubai Financial

Services Authority ("DFSA") (Level 13, West Wing, The Gate,

DIFC) in accordance with Art. 48 of the Regulatory Law 2004. The services

provided by PIMCO Europe GmbH are available only to professional clients as

defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are

not available to individual investors, who should not rely on this

communication. According to Art. 56 of Regulation (EU) 565/2017, an

investment company is entitled to assume that professional clients possess

the necessary knowledge and experience to understand the risks associated

with the relevant investment services or transactions. Since PIMCO Europe

GMBH services and products are provided exclusively to professional clients,

the appropriateness of such is always affirmed. PIMCO (Schweiz) GmbH

(registered in Switzerland, Company No. CH-020.4.038.582-2,

Brandschenkestrasse 41 Zurich 8002, Switzerland). According to

the Swiss Collective Investment Schemes Act of 23 June 2006 ("CISA"), an

investment company is entitled to assume that professional clients possess

the necessary knowledge and experience to understand the risks associated

with the relevant investment services or transactions. Since PIMCO (Schweiz)

GmbH services and products are provided exclusively to professional clients,

the appropriateness of such is always affirmed. The services provided by

PIMCO (Schweiz) GmbH are not available to retail investors, who should not

rely on this communication but contact their financial adviser.

PIMCO Asia Pte Ltd (8 Marina View, #30-01, Asia Square

Tower 1, Singapore 018960, Registration No. 199804652K) is regulated by the

Monetary Authority of Singapore as a holder of a capital markets services

licence and an exempt financial adviser. The asset management services and

investment products are not available to persons where provision of such

services and products is unauthorised. | PIMCO Asia Limited

(Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance

Street, Central, Hong Kong) is licensed by the Securities and Futures

Commission for Types 1, 4 and 9 regulated activities under the Securities

and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border

discretionary investment manager with the Financial Supervisory Commission

of Korea (Registration No. 08-02-307). The asset management services and

investment products are not available to persons where provision of such

services and products is unauthorised. | PIMCO Investment Management

(Shanghai) Limited. Office address: Suite 7204, Shanghai Tower,

479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social

credit code: 91310115MA1K41MU72) is registered with Asset Management

Association of China as Private Fund Manager (Registration No. P1071502,

Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508,

AFSL 246862. This publication has been prepared without taking into account

the objectives, financial situation or needs of investors. Before making an

investment decision, investors should obtain professional advice and

consider whether the information contained herein is appropriate having

regard to their objectives, financial situation and needs. To the extent it

involves Pacific Investment Management Co LLC (PIMCO LLC) providing

financial services to wholesale clients, PIMCO LLC is exempt from the

requirement to hold an Australian financial services licence in respect of

financial services provided to wholesale clients in Australia. PIMCO LLC is

regulated by the Securities and Exchange Commission under US laws, which

differ from Australian laws. | PIMCO Japan Ltd, Financial

Instruments Business Registration Number is Director of Kanto Local Finance

Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of

Japan Investment Advisers Association, The Investment Trusts Association,

Japan and Type II Financial Instruments Firms Association. All investments

contain risk. There is no guarantee that the principal amount of the

investment will be preserved, or that a certain return will be realized; the

investment could suffer a loss. All profits and losses incur to the

investor. The amounts, maximum amounts and calculation methodologies of each

type of fee and expense and their total amounts will vary depending on the

investment strategy, the status of investment performance, period of

management and outstanding balance of assets and thus such fees and expenses

cannot be set forth herein. | PIMCO Taiwan Limited is an

independently operated and managed company. The reference number of business

license of the company approved by the competent authority is (112) Jin Guan

Tou Gu Xin Zi No. 015. The registered address of the company is 40F., No.68,

Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan

(R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO

Canada Corp. (199 Bay Street, Suite 2050, Commerce Court

Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only

be available in certain provinces or territories of Canada and only through

dealers authorized for that purpose. | Note to Readers in

Colombia: This document is provided through the representative

office of Pacific Investment Management Company LLC located at Carrera 7 No.

71-52 TB Piso 9, Bogota D.C. (Promoción y oferta de los negocios y servicios

del mercado de valores por parte de Pacific Investment Management Company

LLC, representada en Colombia.). Note to Readers in Brazil:

PIMCO Latin America Administradora de Carteiras Ltda.Av. Brg. Faria Lima,

3477 Itaim Bibi, São Paulo - SP 04538-132 Brazil. Note to Readers in

Argentina: This document may be provided through the

representative office of PIMCO Global Advisors LLC AVENIDA CORRIENTES, 299,

Buenos Aires, Argentina. | No part of this publication may be reproduced in

any form, or referred to in any other publication, without express written

permission. PIMCO is a trademark of Allianz Asset Management of America LLC

in the United States and throughout the world. ©2025,

PIMCO.

CMR2025-0716-4670668