PIMCO Washington Watch: Tariff Man Shows Up on “Liberation Day”

Thursday, April 3 2025

- What is happening? For those who were hoping that “Liberation Day” may be more bark than bite and might abate some of the rising tariff uncertainty seen in the markets and the soft-data, they arguably got something very different yesterday than what they had hoped for.

- Indeed, in what one Trump staffer referred to as a “glorious day,” President Trump announced a universal baseline tariff of 10% on all imports into the U.S., employing the same emergency powers he used to impose tariffs on Canada and Mexico – “IEEPA” – which could incidentally be legally vulnerable given what many think is an extraordinary (and aggressive) reading of the statute.

- For those countries with whom the U.S. has large goods trade deficits, Trump announced even higher reciprocal tariffs – up to 50% tariffs (here is looking at you, Lesotho). Under the order, EU goods will be tariffed at 20%, Vietnam at 46%, Japan at 24%, and India at 26%.

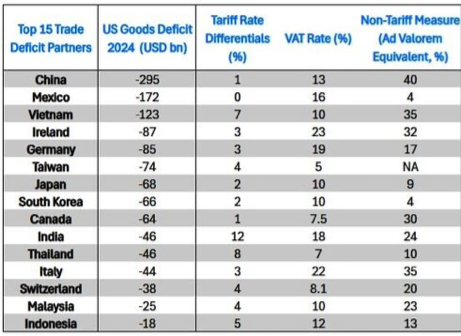

- The biggest loser? Importantly, as it relates to U.S. imports of Chinese goods (~$490bn as of 2024 here), on which Trump had already imposed a 20% tariff, the newly announced 34% reciprocal tariff on China is additional or “stacking,” meaning the minimum tariff on Chinese products will now be 54% (and even higher for products already affected by the 2018 Section 301 tariffs - yikes). It also appears the White House is moving forward with addressing the de minimis loophole for lower valued Chinese goods, which is likely to impact Amazon and Temu (here).

- Wonk alert: For those “high trade deficit” countries, the Trump administration is not determining the individualized reciprocal tariffs on the actual tariffs (or VAT) the countries charge the U.S., but instead on the size of the U.S. goods trade deficit with the specific country divided by what the U.S. imports from that country. For instance, the U.S. has an $18bn goods trade deficit with Indonesia and imports $28bn from Indonesia in goods or $18bn/$28bn = 64%; Trump is halving that rate to get to the 32% tariff the U.S. will now charge on Indonesia While this may make some folks incredulous, this reinforces Trump’s (longstanding) focus on the goods trade deficit. This also may make off-ramps/de-escalation harder since it means that countries cannot simply reduce tariffs on the U.S., but will actually have to decrease their own trade surplus with the U.S., which could take longer than a reduction in tariffs.

- Same as it ever was: Consistent with what Trump was saying back in the 1980s. It is instructive to read the executive order here in which President Trump reinforces what he has literally been saying for decades about trade deficits and tariffs. For instance, there is an entire section entitled “Tariffs Work” in which he expands: “Studies have repeatedly shown that tariffs can be an effective tool for reducing or eliminating threats that impair U.S. national security and achieving economic and strategic objectives;” the EO also talks about “The Golden Rule: Today’s action simply asks other countries to treat us like we treat them.”

- But, but, but: There were some silver linings for those who wanted to see some tariff relief (or least less bad news depending on the perspective). For one, already-tariffed products like autos, aluminum, and steel (as well as forthcoming “section 232” tariffs on pharma, copper, chips, etc.) will not be subject to additional reciprocal tariffs for now (i.e., no stacking of tariffs on those products).

- And two (and significantly), there will be no reciprocal tariffs imposed on Canada or Mexico in addition to those 25% tariffs announced on March 4th (unlike China, where there will be stacking tariffs). Further, the carve-out from the tariffs for USMCA-compliant goods (~50% of goods) will continue, and there is a clear off-ramp for both Canada and Mexico: The EO says that if progress is made on the border and fentanyl, tariffs would decrease to 12% on those countries. (This is significant for the U.S. given how entrenched the supply chains are.)

- What does this mean for the effective U.S. tariff rate? We had been penciling-in an increasingly-higher effective tariff rate over the past few weeks and recently had upsized it to a ~10% increase (notably, most Wall Street firms were barely penciling in any tariffs at the beginning of 2024; we had been, but arguably we were too low as it turns out). Yesterday’s tariffs in addition to the other tariffs Trump has announced could increase the effective tariff rate by as much as 25% (assuming the pharma, CHIPS tariffs go on), which would be the highest tariffs the country has seen in nearly 100 years. Other estimates range from Evercore at 30% to Goldman which is ~18%.

- What does this mean for growth and inflation? If these tariffs stay on, according to Tiffany, we could see growth decline to ~0% over the next year and inflation increase to 4.5%, if not higher, with recession probabilities increasing and a potential negative impact on the labor market likely; all of this could lead the Fed to cut even more this year (which explains the market reaction). This obviously depends on the reaction function of other countries, however in terms of retailiation.

- A rule of thumb is that for every 1% increase of the U.S. effective tariff rate , there is a ~.1% headwind to growth and +.1% read-through to inflation. Of course, there are a lot of assumptions embedded in this (e.g., FX movement, the extent to which countries retaliate, etc.), but nevertheless, it is a handy approximation.

- What is next? Trump warned that if countries retaliate, the U.S. will also retaliate: “Should any trading partner retaliate against the United States in response to this action through import duties on U.S. exports or other measures, I may further modify the [order] to increase or expand in scope the duties imposed under this order to ensure the efficacy of this action.” He also warned: “Should U.S. manufacturing capacity and output continue to worsen, I may further modify the order to increase duties.”

- At the same time, Trump opened the door to negotiations and to deals: “Should any trading partner take significant steps to remedy non-reciprocal trade arrangements and align sufficiently with the United States on economic and national security matters, I may further modify the [order] to decrease or limit in scope the duties imposed.”

- The biggest question clients are asking is what is Trump’s pain tolerance – i.e., how long will Trump stick with tariffs and what could be the catalyst for a pivot. Clearly the assumption that many had that Trump would be highly sensitive to any drawdown in the equity market has not held-up (we were dubious of that pervasive assumption anyway). At the same time, he is certainly not entirely impervious to a market decline, nor is he unaffected by public sentiment, significant Congressional pushback, or concerns about a recession. So, there is likely a limit to how much pain he and his administration are willing to endure in order to rebalance the economy, but when that is or what that looks remains to be seen. For now, we should assume that his pain tolerance is pretty high and that tariffs stick around for a while.

- Bottom line: Trump 2.0 has been maximalist in most every way, and trade policy is no exception. Anyone who may have doubted Trump’s seriousness about rebalancing the economy through tariffs and his deeply held belief that tariffs work, should be convinced by now. While we would expect Trump to soften at least some of these tariffs at some point, what the limit – political or otherwise – for him to pivot to do that remains to be seen. Assuming the tariffs stay on – even for a few quarters – we should expect to see economic damage both in terms of a drag on growth, maybe even tipping into recession, and upward pressure on inflation. At the same time, we may see Trump lean into the tax cuts – the proverbial dessert – which could be accelerated and be bigger than originally thought as an effort to give the market what would be very welcome dessert after a strict diet of veggies so far.

PIMCO Washington Watch: All About “Liberation Day”

Monday, March 31 2025

- What is happening? This week will include “Liberation Day,” (April 2nd) on which President Trump plans to announce additional tariff measures, including the much-touted reciprocal tariffs, but the exact scope, severity, and timing all remain open questions (even to folks in or close to the White House).

- As of last week, Trump described the imminent tariffs as “more lenient” and “generous” than what people may expect (here), while yesterday, he indicated that “all trading partners” may be impacted, and according to the WSJ, is contemplating a more draconian across-the-board (“universal”) 20% tariff, rather than the more tailored (and by definition, lower) “reciprocal” tariffs (here). As discussed below, the legality behind universal tariffs may ultimately dissuade the president from proceeding.

- Also, this week will see special elections in Florida for two seats in the House of Representatives to fill the seat of (now well-known) National Security Advisor and former member of the House, Mike Waltz, as well as the seat of Matt Gaetz (here). Both seats should be easy for Republicans to maintain; after all, Gaetz’s district is one of the most conservative in Florida (and in the country) while Waltz won his House race with 67% of the vote. The race to replace Waltz, in particular, has attracted national attention given both candidates have raised a lot of money, but Democrats’ hope to flip a very red district seems unlikely (although in this political environment, never say never).

- Back to “tariff man:” As a reminder, at the beginning of his term, the April 1st / 2nd dates were intended, in some ways, to be the great reveal of Trump’s trade agenda as outlined in his America First Trade Policy Executive Order, but over the past 70 days, we have seen Trump front-run that executive order and announce and impose several rounds of tariffs, including:

- 20% additional tariffs on all Chinese goods (February 4; March 4)

- 25% tariff on Canada and Mexico goods, 10% on energy (March 4); later amended to only apply to non-USMCA-compliant goods (about ~50% of products as of now, but will decrease as exporters seek compliance)

- 25% tariffs on steel and aluminum (March 12)

- 25% on autos and auto parts with few exceptions (effective April 3)

- A rule of thumb? Needless to say, these tariff actions collectively are much more substantial than Trump 1.0 tariff measures and have already increased the “effective tariff rate” by ~6%; a rule of thumb is that there is a .1%-.15% pass-through as a negative growth shock for every percent the effective tariff rate increases and about the same for inflation. In other words, a 6% increase would lead to ~.6-.9% headwind to growth and a similar upward pressure on CPI. This is all approximate of course (and makes assumptions about FX, retaliation, etc.) but it is a good approximation.

- Yes, and: Trump has announced that he will do even more as of Wednesday, which could impede growth further depending on the tariffs; durability; those are likely to include:

- 20% universal tariffs on all trading partners; this would be more significantly inflationary as well as a headwind to growth; or,

- Loaded “reciprocal tariffs” calculated to include both the tariffed country’s tariff rate as well as other “non-trade barriers,” including the VAT (see below for the extent of these non-tariff barriers numerically); this would be less impactful than the universal tariff but still would bite from an economic perspective; or,

- Simple reciprocal tariffs determined by the tariff rate; this is the least impactful from a macroeconomic perspective and is probably the least likely as well.

- Product-specific tariffs: President Trump has also indicated he will impose product-specific tariffs on CHIPS ($140bn of imports) and pharmaceuticals ($250bn of U.S. imports) as well as on lumber, copper, and ships. This plus the tariffs on the autos would raise the “effective tariff rate” by another 3-4% alone and be another headwind to growth of ~.5% or so.

- But, but, but: While there be significant headlines on Wednesday, a key question surrounds the timing – when will the tariffs actually be imposed? Is this “escalate to deescalate” (i.e., give time for countries to negotiate before tariffs roll-on, if at all), or do tariffs roll-on immediately, leaving little room to negotiate or for a deal?

- Legal authority matters: Which legal or statutory authority the president uses to impose tariffs may sound tedious, but it is quite important as it will dictate how immediate the tariffs can roll-on and how durable they are in court when they are imposed. Some examples include:

- International Emergency Economic Powers Act (IEEPA): This allows the president wide-ranging authorities in the event of an economic emergency (defined quite subjectively) and could allow Trump to impose a universal tariff or reciprocal tariff immediately (this is how he imposed the tariffs on Mexico and Canada citing an economic emergency on the border and on fentanyl). From what we understand, the White House lawyers would expect this to be litigated, however, so may not be that appealing to impose either a universal or reciprocal tariffs.

- Section 301, 1974 Trade Act: This requires a lengthy investigation but once the findings are conclusive, it allows the president to impose tariffs that are likely to have durability in the courts (this is how the U.S. imposed China tariffs under Trump 1.0). This could be the preferred way for the legal counsel, but it would take time – ~3-9 months to complete one investigation and is likely take too much time for the president. There is an open investigation on France’s digital service tax (from Trump 1.0) so we may see something announced on this at some point.

- Section 338, 1930 Tariff Act: This also be the legal way in which Trump puts reciprocal tariffs on, but would almost certainly be litigated. This authority has not been used since the 1930s, and given a lot in trade law has evolved since then, a plaintiff would likely have a pretty good case to litigate it.

- Section 122, 1974 Trade Act: This allows the president to move forward if there is a “balance of payments” crisis, which could be the legal cover for reciprocal (or universal) tariffs. However, there are certain limitations to this, including timing (can only be put on for 150 days with Congressional approval) and scope (15% is the limit).

- Section 232, 1962 Trade Act: This is the authority that was used to move forward with both autos and steel/aluminum and steel over the past few weeks, but Trump was only able to do so immediately given there were open investigations on steel and autos from Trump 1.0. This is likely the authority that Trump uses to impose tariffs on pharma, chips, and other products, but by definition, these investigations take time, and while they could be announced this week, it is unlikely they are imposed this week.

- Bottom line: While the executive branch has broad authorities to impose tariffs, it is unclear how -or which statute – Trump will use to proceed with his reciprocal (or universal) tariffs, which may have a practical impact on the timing of the tariffs as well as the durability (especially if he uses IEEPA). Regardless, the effective tariff rate has already increased significantly and could increase even more – our base case is ~9-10% but we could easily see these tariff actions surpass that, which could be a bigger headwind to growth 1-1.5% of growth) as well to the Fed’s objective of getting closer to 2% inflation. Of course, the economic impact all depends on the stickiness of these tariffs, when they are applied, and their legal durability.

In general, as we have said before, we believe that Trump thinks that tariffs are both a means to an end (extracting concessions from trading partners) as well as an end in and of themselves (e.g., rebalancing trade and increasing investment in the U.S., raising revenues for the U.S.). Additionally, President Trump has said – and seems to ardently believe – that tariffs are a solution, rather than what the market thinks they are (a problem). While the rapidity at which Trump has imposed tariffs has been impressive, in some ways, it should not surprising given his world view and the sense of finished business from Trump 1.0. In other words, while the market seems to have a desire to think Trump is more bark than bite on tariffs, our view is there is a lot more ideologically-driven bite than many had assumed. The upshot is that while we will likely get clarity this week on tariffs, we will very likely be living with trade policy uncertainty – and significantly higher effective tariffs rates – for the rest of Trump 2.0.

Source: Bloomberg

Libby Cantrill, CFA

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission.| PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963, via Turati nn. 25/27 (angolo via Cavalieri n. 4), 20121 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain) and PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50–52 Boulevard Haussmann, 75009 Paris, France) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch, UK Branch, Spanish Branch and French Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively and (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. According to Art. 56 of Regulation (EU) 565/2017, an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO Europe GMBH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2, Brandschenkestrasse 41 Zurich 8002, Switzerland). According to the Swiss Collective Investment Schemes Act of 23 June 2006 (“CISA”), an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO (Schweiz) GmbH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (8 Marina View, #30-01, Asia Square Tower 1, Singapore 018960, Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited (Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance Street, Central, Hong Kong) is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Investment Management (Shanghai) Limited. Office address: Suite 7204, Shanghai Tower, 479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social credit code: 91310115MA1K41MU72) is registered with Asset Management Association of China as Private Fund Manager (Registration No. P1071502, Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. To the extent it involves Pacific Investment Management Co LLC (PIMCO LLC) providing financial services to wholesale clients, PIMCO LLC is exempt from the requirement to hold an Australian financial services licence in respect of financial services provided to wholesale clients in Australia. PIMCO LLC is regulated by the Securities and Exchange Commission under US laws, which differ from Australian laws. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association, The Investment Trusts Association, Japan and Type II Financial Instruments Firms Association. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is an independently operated and managed company. The reference number of business license of the company approved by the competent authority is (112) Jin Guan Tou Gu Xin Zi No. 015 . The registered address of the company is 40F., No.68, Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan (R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | Note to Readers in Colombia: This document is provided through the representative office of Pacific Investment Management Company LLC located at Carrera 7 No. 71-52 TB Piso 9, Bogota D.C. (Promoción y oferta de los negocios y servicios del mercado de valores por parte de Pacific Investment Management Company LLC, representada en Colombia.). Note to Readers in Brazil: PIMCO Latin America Administradora de Carteiras Ltda.Av. Brg. Faria Lima, 3477 Itaim Bibi, São Paulo - SP 04538-132 Brazil. Note to Readers in Argentina: This document may be provided through the representative office of PIMCO Global Advisors LLC AVENIDA CORRIENTES, 299, Buenos Aires, Argentina. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2025, PIMCO.

CMR2025-0403-4376314