Macro Signposts | 10 December 2024

This week, I asked members of PIMCO's real return portfolio management team to guest author Macro Signposts and share their insights into global inflation trends.

Global Inflation: Is the Tide Turning?

By Steve Rodosky and Daniel He

U.S. inflation has dropped from a staggering peak of 9.1% during the height of COVID-19 to a more manageable 2.6% as of October 2024, as measured by the headline Consumer Price Index (CPI). This dramatic shift raises important questions about the trajectory of inflation: Are we on the cusp of a return to the golden era of low and stable inflation that characterized the economy from the 1990s to the mid-2010s? Or are we reverting to a historical norm marked by inflation averaging above 2% and heightened volatility?

The upshot is we believe the tide has most likely turned: Inflation may be more volatile and linger above central bank targets. Several global macroeconomic trends drive this view. And for investors, this means assessing portfolios' resilience to inflation - and to inflation surprises. Real assets, such as inflation-linked bonds, may offer attractive real yields and inflation hedging.

The golden era of low and stable inflation

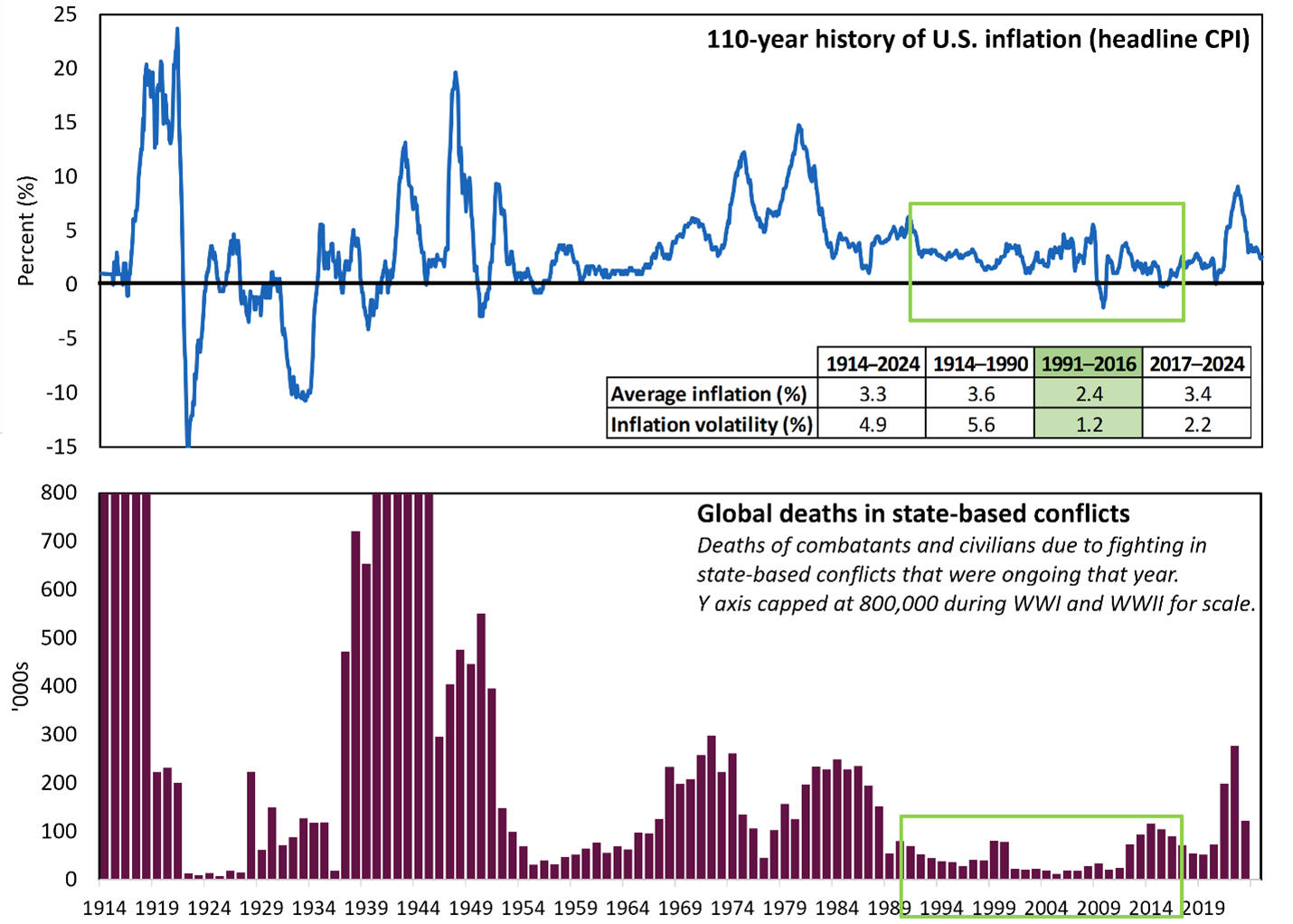

The period from 1990s to mid-2010s had remarkably low headline inflation in the U.S., averaging just 2.4% (see Figure 1). This compares with an average inflation rate of 3.6% over the 75 years prior and 3.4% since 2016. More remarkably, the volatility of inflation during this period was a mere 1.2%, versus 5.6% and 2.2% in the other two periods. When viewed from the lens of a 110-year history, the era of calm appears more as an anomaly than a standard (see Figure 1, top panel).

Figure 1: 110-year history of U.S. inflation and global conflicts

|

Source: Bloomberg data, OurWorldinData.org, Uppsala Conflict Data Program, Peace Research Institute Oslo, and PIMCO calculations as of 31 October 2024

A closer examination of this unique period reveals key macro trends underpinning lower inflation.

The years leading up to 2016 were marked by a significant degree of global peace, with the lowest number of deaths in history from state-based conflicts. (see Figure 1, bottom panel). This environment coincided with a period of international cooperation and stability - including accelerated globalization. This trend started with the end of the Cold War in 1991 and signing of the Maastricht Treaty in 1992, establishing the European Union. The North American Free Trade Agreement went into effect in 1994, soon followed by the formation of the World Trade Organization (WTO) a year later. The arguable pinnacle of globalization was China's accession to the WTO in 2001, unleashing "the factory of the world."

The reduced levels of global conflict and the higher levels of trade integration may have bolstered each other in a self-stoking cycle. Overall, this extended period of relative peace and globalization supported economic growth, stabilized (or lowered) the prices of many goods, and helped tame inflation volatility.

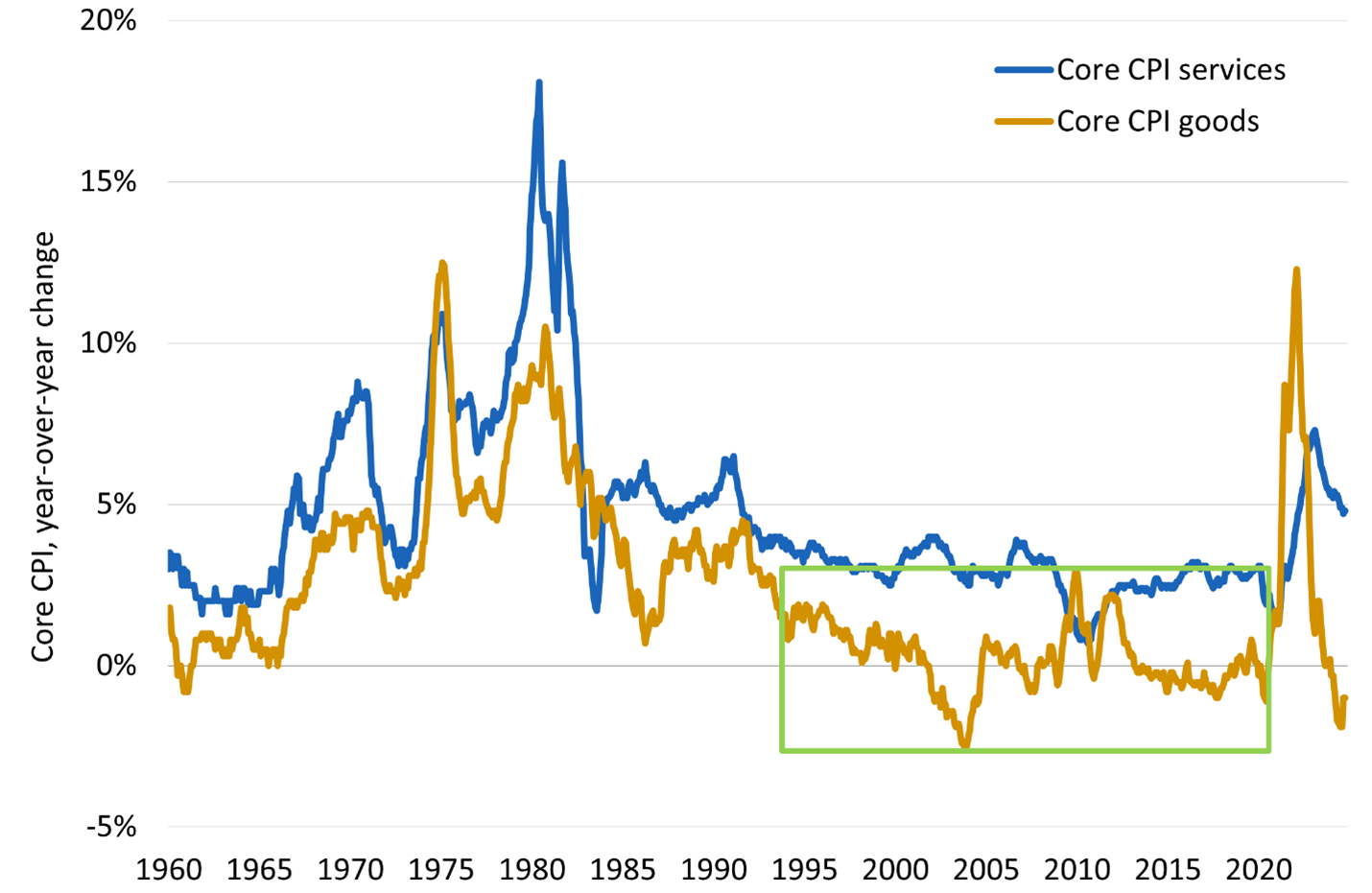

During this time, world imports of goods and services increased from 18% of total world GDP to 30% of GDP, according to the World Bank. In fact, after China started producing for the world within the WTO, goods inflation in the U.S. went negative before hovering near zero. Because services inflation remained well above 2%, goods disinflation was the key to keeping overall U.S. inflation low throughout the period (see Figure 2).

Figure 2: Goods disinflation vs. services inflation in the U.S.

|

Source: Bloomberg data and PIMCO calculations as of 31 October 2024

The golden era ends

Just as it seemed that we had found the perfect formula for keeping global inflation low and stable, conditions began to turn. The rise of populist political movements globally, exemplified by the Brexit referendum in 2016, marked a departure from the cooperative spirit of the previous decades. The U.S.-China trade war in 2018 symbolically rang the opening bell for deglobalization. The COVID-19 pandemic and Russia-Ukraine war further disrupted global supply chains and prompted many countries to reconsider their reliance on global trade. That led to further momentum in near-shoring and friend-shoring. By 2023, Mexico overtook China as the top exporter to the U.S., according to the U.S. Census Bureau, for the first time since 2004 (shortly after China joined the WTO).

Moreover, the world is now experiencing more conflicts than at any time in the past 30 years, ending the peace dividend that had previously fostered cooperation and suppressed inflation (Figure 1, bottom panel). Just as globalization and peace tended to grow in tandem during the golden era, so might deglobalization and conflict in the years to come.

What lies ahead for inflation?

The reversal of conditions means we could stay in a higher inflation and higher volatility world. The trend of goods disinflation that characterized the previous era is likely coming to an end as deglobalization takes hold. Simultaneously, services inflation may be boosted by populist anti-immigration policies, potentially leading to less labor supply and higher prices.

In the near term - or longer, depending on future governments - fiscal policies, trade policies, and geopolitical tensions also pose significant risks to inflation. With the U.S. fiscal deficit projected to remain above 6% (according to the Congressional Budget Office), and the potential for tariffs to increase significantly across the board (as U.S. President-elect Donald Trump has indicated he intends to do), the inflation landscape is fraught with uncertainty. Additionally, geopolitical risks in Europe, the Middle East, and Asia - particularly concerning Taiwan - could disrupt supply chains and accelerate inflation.

Central banks will seek to keep inflation (and inflation expectations) near target via ordinary and perhaps extraordinary means, but these global trends could pose clear challenges.

Investment implications

The potential return of elevated inflation volatility carries several important implications.

Long-term breakeven inflation rates are currently priced at 2.3% (according to Bloomberg), exactly the same as the average inflation during the golden era (and just above the Federal Reserve's target), indicating a lack of risk premium despite recent inflation spikes, the near-term inflation risks, and a potential return to a higher inflation and higher volatility regime. As inflation surprises become more likely, the risk premium should rise.

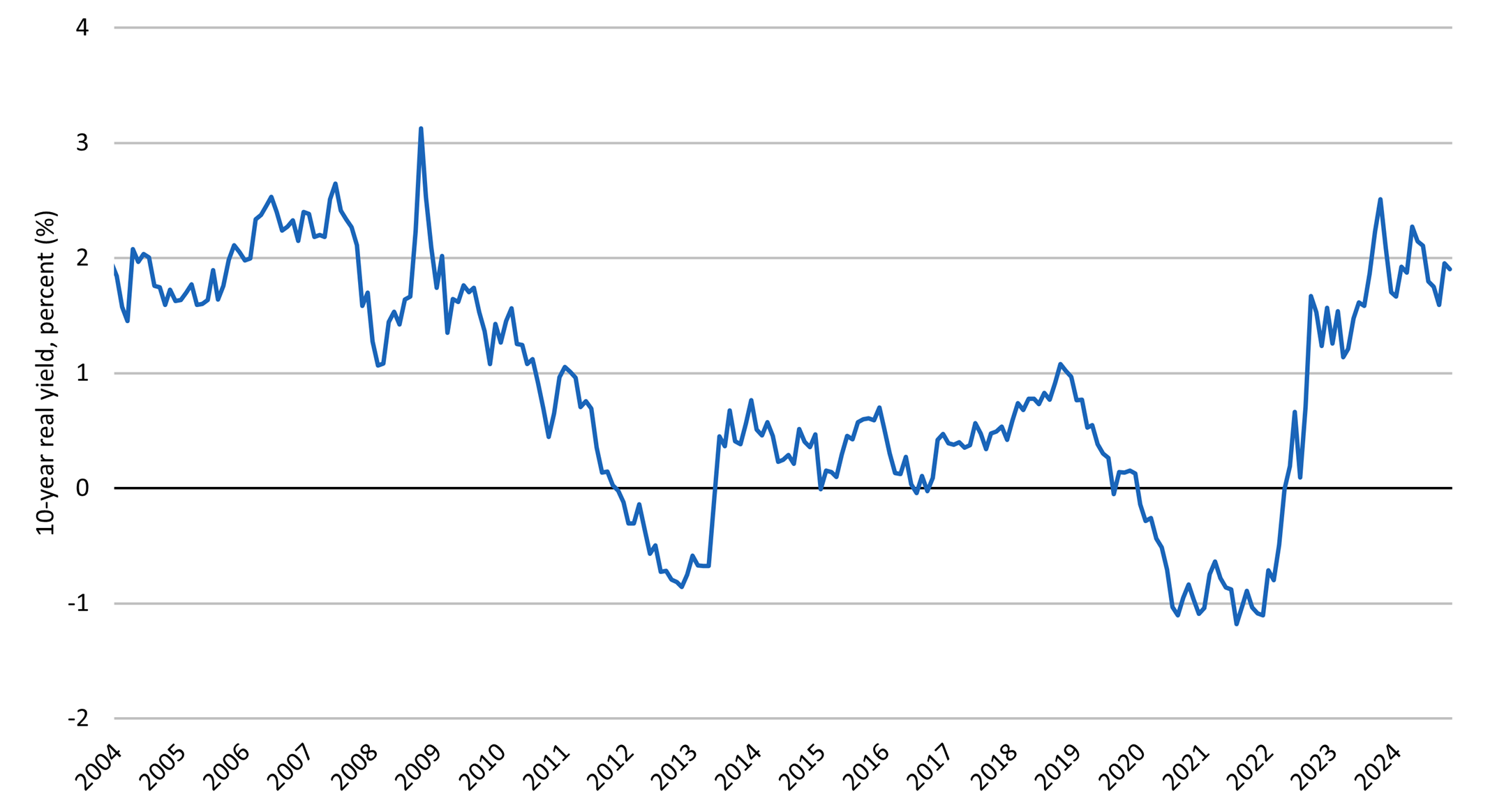

Given the evolving inflation landscape, investors may need to reassess their strategies. Real yields on U.S. Treasury Inflation-Protected Securities (TIPS) are currently at 15-year highs (see Figure 3), exceeding the Fed's model estimates of neutral rates by 75-125 basis points (according to the New York Fed), presenting an attractive opportunity for those seeking to hedge inflation.

Figure 3: Real yield on 10-year U.S. TIPS at 15-year high

|

Source: Bloomberg data as of 29 November 2024

A multi-faceted approach to real asset hedging could significantly enhance portfolio resilience in the face of potentially rising inflation and increased volatility. Learn more in our recent article on real assets.

Catch up on recent editions of Macro Signposts:

- U.S. Debt Dilemma: Politics and Economics | 27 November 2024

- Fed 2025 Outlook: Hikes Still Unlikely | 20 November 2024

- Economic Changes That U.S. Voters Want to See | 14 November 2024

- Key Policy Questions for the U.S. Economic Outlook | 5 November 2024

- How Will Markets Respond to the U.S. Election? | 30 October 2024

Macro Signposts highlights weekly takeaways from the data analysis conducted by our team of economists and other macro experts. For PIMCO's official views on the global economy, please visit pimco.com.

We welcome your questions about the global macro landscape. Don't hesitate to suggest themes or data for us to analyze and discuss: Please email [email protected].

For regular insights on U.S. policy via email, please sign up here to receive PIMCO Washington Watch from Libby Cantrill, head of public policy.

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

This material contains the current opinions of the author and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. | PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. Since PIMCO Europe Ltd services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963, via Turati nn. 25/27 (angolo via Cavalieri n. 4), 20121 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain) and PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50-52 Boulevard Haussmann, 75009 Paris, France) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch, UK Branch, Spanish Branch and French Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively and (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. According to Art. 56 of Regulation (EU) 565/2017, an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO Europe GMBH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2, Brandschenkestrasse 41 Zurich 8002, Switzerland). According to the Swiss Collective Investment Schemes Act of 23 June 2006 ("CISA"), an investment company is entitled to assume that professional clients possess the necessary knowledge and experience to understand the risks associated with the relevant investment services or transactions. Since PIMCO (Schweiz) GmbH services and products are provided exclusively to professional clients, the appropriateness of such is always affirmed. The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (8 Marina View, #30-01, Asia Square Tower 1, Singapore 018960, Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited (Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance Street, Central, Hong Kong) is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Investment Management (Shanghai) Limited. Office address: Suite 7204, Shanghai Tower, 479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social credit code: 91310115MA1K41MU72) is registered with Asset Management Association of China as Private Fund Manager (Registration No. P1071502, Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. To the extent it involves Pacific Investment Management Co LLC (PIMCO LLC) providing financial services to wholesale clients, PIMCO LLC is exempt from the requirement to hold an Australian financial services licence in respect of financial services provided to wholesale clients in Australia. PIMCO LLC is regulated by the Securities and Exchange Commission under US laws, which differ from Australian laws. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association, The Investment Trusts Association, Japan and Type II Financial Instruments Firms Association. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is an independently operated and managed company. The reference number of business license of the company approved by the competent authority is (112) Jin Guan Tou Gu Xin Zi No. 015. The registered address of the company is 40F., No.68, Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan (R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | Note to Readers in Colombia: This document is provided through the representative office of Pacific Investment Management Company LLC located at Carrera 7 No. 71-52 TB Piso 9, Bogota D.C. (Promoción y oferta de los negocios y servicios del mercado de valores por parte de Pacific Investment Management Company LLC, representada en Colombia.). Note to Readers in Brazil: PIMCO Latin America Administradora de Carteiras Ltda.Av. Brg. Faria Lima, 3477 Itaim Bibi, São Paulo - SP 04538-132 Brazil. Note to Readers in Argentina: This document may be provided through the representative office of PIMCO Global Advisors LLC AVENIDA CORRIENTES, 299, Buenos Aires, Argentina. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2024, PIMCO.

CMR2024-1209-4084599