Macro Signposts | 21 February 2024

Unless explicitly stated, views expressed do not constitute official PIMCO views.

Why Rent Levels May Not Drive Rapid U.S. Disinflation

Last week, the annual policy conference of the National Association for Business Economics (NABE) in Washington, D.C., hosted Fed and Treasury officials, along with hundreds of economists, analysts, and business leaders. I participated in a panel on the Fed's balance sheet, but the most intriguing takeaways came from conversations on the sidelines. What surprised me was the overwhelming consensus that rents would drive another rapid disinflation in the U.S. economy in 2024.

Key to this argument is the collapse in market rents in multifamily structures. Many economists at the conference suggested the Fed should already be considering rate cuts because this trend suggests inflation is headed sustainably toward the central bank's target.

As Macro Signposts regulars may guess, we think the outlook for inflation is more nuanced. We agree that inflation in owners' equivalent rent (OER) – the largest component of core CPI at 24% – will likely continue to moderate. However, its path is likely to be slower and "bumpier," like the unexpected jump in January OER, than many expect. We point to three reasons.

Important distinctions in measurement: markets vs. OER average

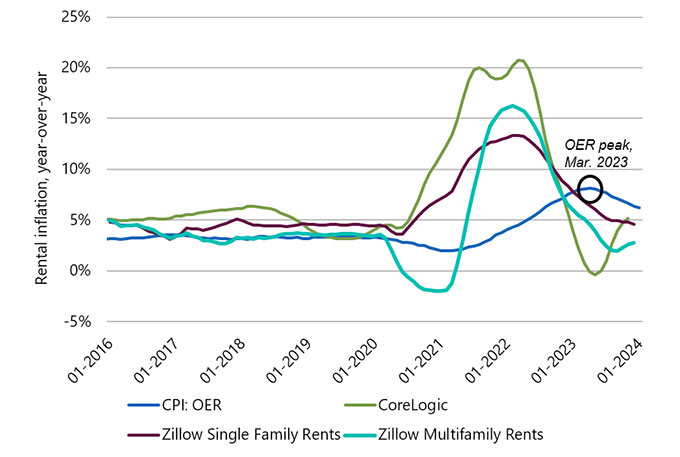

First, it's important to differentiate between measures of rents. Market measures of rent represent the marginal rent paid by the next renter. In contrast, OER reflects the average rent paid across a representative sample of units – including those that do not come to market.

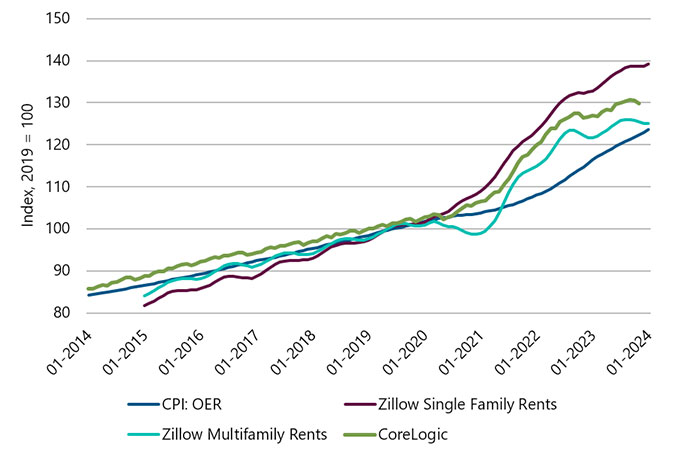

This distinction is important: Although inflation in market rents – which has tended to lead OER inflation by around 1 year (see Figure 1) – has dipped below pre-pandemic levels, there still exists a relatively large 5%–10% gap between the levels of market and average rents (see Figure 2). In essence, most renters pay below-market rents due to locked-in contracts or capped increases. This gap should support OER inflation over time – and moderate OER inflation more slowly than if the gap didn't exist.

| Figure 1: Market rent measures tend to lead OER |

|

| Source: U.S. Bureau of Labor Statistics (BLS) CPI OER data through January 2024; Zillow data through December 2023; CoreLogic data through November 2023 |

| Figure 2: Single family home rents remain particularly high |

|

| Source: U.S. Bureau of Labor Statistics (BLS) CPI OER data and Zillow data through January 2024; CoreLogic data through November 2023. All measures are indexed to 100 in 2019. |

According to 2023 research by Brian Adams of the Bureau of Labor Statistics (BLS) (et al.), published by the Cleveland Fed, only an estimated 10%–20% of the CPI rental sample is based on new tenant rents, implying that it may take 4 years at least before the average rents of the outstanding rental stock catch up to the new lease rents, assuming new lease rents don't rise further. Put another way, unless national market rents fall 5%–10% (which is unlikely outside a recession), non-market rents (and therefore OER) are likely to continue to be supported by landlords trying to "catch up" to market rates.

Single family rents remain firm

Second, rents of single family detached structures – the majority of the OER sample – are still much firmer than multifamily apartment units. This will tend to make OER inflation slower to moderate than the CPI "rent" measure, which is 8% of CPI, and where multifamily properties are a larger portion of the sample base. A 2020 paper1 by Brian Adams and Randal Verbrugge found a high degree of rental market price segmentation, especially between single family detached housing and large multifamily apartment buildings. The findings were so conclusive that in January 2023, the BLS updated its OER sample2 to better represent rental trends in the single family housing market.

Pandemic-related trends in housing markets increased the importance of the BLS's move to increase the weight of single family structures toward 90% (from around 50% previously). The wave of migration from city centers during the pandemic pushed up rents of single family homes by around 10 percentage points more than rents of multifamily structures, on a cumulative basis since 2019, according to Zillow.

More recently, rents in multifamily structures have declined as a large amount of supply has come to market, especially in cities across the sunbelt. And with more multifamily rental unit supply expected in 2024, the outlook for prices of multifamily structures is likely to remain subdued. Nevertheless, prices of single family detached structures appear generally more stable and above pre-pandemic levels, implying any OER inflation moderation will lag behind many predictions based on pre-2023 CPI rental sample weights.

These differences in rental trends between single family and multifamily also appear to be driving the underperformance in the BLS's "New Tenant Rent Index." The index collapsed in Q4 2023, leading some market commentators to argue that OER will soon follow. We aren't so sure. The measure has a relatively small sample size (which is even smaller in Q1, when few people change residences) of mostly multifamily units, which tend to turn over with new tenants more frequently. The fact that OER has been firm despite the collapse in this measure implies that strength in other segments of the rental market is more than offsetting this weakness.

It's hard to buy a home

Third, buying a home in the U.S. is still much less affordable, despite the recent fall in 30-year fixed mortgage rates from a peak of roughly 8% last October to just above 7% today. This should keep rents high and rising as more people who can't afford to buy opt to rent instead. Since 2019, the average monthly payment on a 30-year fixed mortgage (assuming a 20% down payment and using the national average home sales price) has jumped almost 70% (from $1,300 to almost $2,300 per month, according to our calculations). Over the same period, market rents for single family properties have increased 40%, according to Zillow, and OER has increased a little over 20%.

Takeaways

What does all of this mean? By our estimation, OER inflation is likely to continue to slowly moderate as pandemic-related effects fade. However, it seems premature to expect a quick return to pre-pandemic rental market trends. Over the next few years, OER inflation is likely to remain supported by higher market rents for single family homes, a catch-up in the average rents paid, and reduced home affordability compared with pre-pandemic levels. It could be well into 2025 before OER more fully adjusts to the post-pandemic reality in rental markets.

Given the recent BLS sampling shifts toward the previously underrepresented single family market, we also suspect the January volatility in OER could continue in future reports. Single family detached structures are harder to find and sample because individual units come to market so infrequently that it's not obvious to a government surveyor it's a rental property. As a result, the BLS will likely continue to increase the importance of the rental signals from the single family units it does manage to sample. This means that fewer numbers of units may drive reported average rent changes in the CPI – a recipe for more volatility.

All of this bolsters the argument that the Fed likely has a "last mile" problem. As we've emphasized in recent publications, the relatively painless disinflation of 2023 is likely to become a slower, more nuanced process in 2024. This doesn't rule out Fed rate cuts, but it means that absent a more material weakening in the economy and labor market, Fed officials may need more data before gaining enough confidence in the outlook for inflation to initiate rate cuts. Subsequent cuts also may progress more slowly than they have during historical average nonrecessionary easing cycles (for details, see Macro Signposts, "Central Bank Cuts: Lessons From History," 19 December 2023).

Read the previous edition of Macro Signposts on higher shipping costs and the potential impact on inflation and monetary policy.

We welcome your questions about the global macro landscape. Don't hesitate to suggest themes or data for us to analyze and discuss: Please email [email protected].

For regular insights on U.S. policy via email, please write to [email protected] and ask to receive the Washington Watch.

1 Brian Adams and Randal Verbrugge, "Location, Location, Structure Type: Rent Divergence within Neighborhoods," U.S. Bureau of Labor Statistics working paper 533, December 2020

2 U.S. Bureau of Labor Statistics notice on the Consumer Price Index, "Recent and upcoming methodology changes: 2022," September 2022

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision. Outlook and strategies are subject to change without notice.

This material contains the current opinions of the author and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. | PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963, via Turati nn. 25/27 (angolo via Cavalieri n. 4), 20121 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain) and PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50–52 Boulevard Haussmann, 75009 Paris, France) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch, UK Branch, Spanish Branch and French Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively and (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2, Brandschenkestrasse 41 Zurich 8002, Switzerland). The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (8 Marina View, #30-01, Asia Square Tower 1, Singapore 018960, Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited (Suite 2201, 22nd Floor, Two International Finance Centre, No. 8 Finance Street, Central, Hong Kong) is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Investment Management (Shanghai) Limited. Office address: Suite 7204, Shanghai Tower, 479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social credit code: 91310115MA1K41MU72) is registered with Asset Management Association of China as Private Fund Manager (Registration No. P1071502, Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. To the extent it involves Pacific Investment Management Co LLC (PIMCO LLC) providing financial services to wholesale clients, PIMCO LLC is exempt from the requirement to hold an Australian financial services licence in respect of financial services provided to wholesale clients in Australia. PIMCO LLC is regulated by the Securities and Exchange Commission under US laws, which differ from Australian laws. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association, The Investment Trusts Association, Japan and Type II Financial Instruments Firms Association. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is an independently operated and managed company. The reference number of business license of the company approved by the competent authority is (112) Jin Guan Tou Gu Xin Zi No. 015 . The registered address of the company is 40F., No.68, Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan (R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | Note to Readers in Colombia: This document is provided through the representative office of Pacific Investment Management Company LLC located at Carrera 7 No. 71-52 TB Piso 9, Bogota D.C. (Promoción y oferta de los negocios y servicios del mercado de valores por parte de Pacific Investment Management Company LLC, representada en Colombia.). Note to Readers in Brazil: PIMCO Latin America Administradora de Carteiras Ltda.Av. Brg. Faria Lima, 3477 Itaim Bibi, São Paulo - SP 04538-132 Brazil. Note to Readers in Argentina: This document may be provided through the representative office of PIMCO Global Advisors LLC AVENIDA CORRIENTES, 299, Buenos Aires, Argentina. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2024, PIMCO.

CMR2024-0222-3406380